Today’s Mortgage Rates updated as of August 6, 2026 4:47 pm

5-year fixed*

5-year Variable*

*Insured loans. Other conditions apply. Rate in effect as of today.

TD Bank is one of Canada’s largest financial institutions, offering a range of competitive mortgage products to meet the needs of homeowners, refinancers, and investors. At Citadel Mortgages, we help you access the best TD Bank mortgage rates, ensuring a seamless experience while securing the perfect mortgage for your needs.

Whether you’re a first-time homebuyer, refinancing, or renewing your mortgage, understanding current trends and available options helps you make informed financial decisions.

This guide focuses on helping you navigate the Canadian mortgage market, offering insights into current rates, strategies for securing the best deal, and regional trends.

Mortgage brokers play a pivotal role in helping Canadians find tailored financing options, providing expert advice, and navigating the often complex mortgage market.

For more detailed information on mortgage types, costs, and rights, consult the Government of Canada – Financial Consumer Agency of Canada (FCAC).

Compare TD mortgage rates to other top lenders to ensure you’re getting the best deal. Contact us to explore all your options.

Learn more about today’s best mortgage rates in Canada.

Prime rates change when the Bank of Canada raises or lowers its overnight rate. When it comes to mortgages, there is a separate mortgage rate that tends to be lower than the prime rate. TD Bank’s prime rate is the highest it’s been since 2001.

5-Year History of TD Prime Rate

To get a feel for changes to the TD prime rate over the years, here is the 5-year history:

TD offers the following mortgage features:

Increase Your Mortgage Payment:

Each year you can make an extra payment for your month of choice. This is an important feature, as it allows you to pay down your mortgage more quickly when you have a little extra cash available. Many mortgages apply a penalty when you wish to make additional payments, which makes this a feature to use as a point of comparison. The payment can be up to the full amount of your usual monthly payment.

Annual Mortgage Prepayment:

Another way TD helps you pay down your mortgage more quickly is their annual mortgage prepayment. This allows you to contribute up to 15% of your original mortgage principal as a lump sum each year on closed mortgages. When you take advantage of this option, you reduce interest paid over the life of your mortgage and become mortgage-free sooner.

Payment Pause:

Over the full amortization period of your mortgage, TD allows you to skip four payments, with a limit of one per year. This means you can’t save them all up and then skip all four at once. These skipped payments are not considered a default held against you and instead act more like a deferral or grace period without a negative impact on your payment history. The payment pause is based on your payment frequency, either a single skipped payment for the month, two skipped payments for bi-weekly, and four skipped payments for weekly. However, when you skip a payment, it’s important to remember it slows down how long it takes to pay off your mortgage. It also costs you more in interest. This is especially true if you take full advantage of the four payment pauses you are allowed to take over the life of your mortgage. This is because TD applies the interest not paid on your skipped payments to your principal balance. It is best to save your paused payments for a rainy day.

Payment Vacation:

In hand with your payment pause option, TD also offers a payment “vacation” for up to four months. This is based on the prepaid amount of your mortgage. It is ideal for scenarios where you need time off work and aren’t earning money, whether it is because you are sick, having a baby, or returning to school. As with the payment pause, be sure this is worth it, because those four months of interest accrue and are applied to your mortgage principal. Also, it will take you at least four months longer to pay off your mortgage, in hand with the time it takes to pay off the extra interest. Although it does make your mortgage a bit more flexible, make sure you understand the pros and cons.

Monthly Property Tax Payments:

Most mortgages require you to pay your property tax along with your mortgage payments. If your mortgage does not, TD offers the option for you to pay towards your property taxes and the money collected they then pay for you when they are due. There really isn’t a big benefit to this, but it’s there if you want it.

Mortgage Protection Insurance:

At the time you sign your mortgage, you can opt-in for mortgage protection insurance. The premiums do not increase over the life of your mortgage, and your insurance offers coverage for various scenarios, such as the death of the policyholder or a critical illness that keeps you from making payments. Mortgage life insurance is always a good idea, as it pays off your mortgage, so the burden of the payments doesn’t fall onto the shoulders of family members. Just keep in mind the premiums add up over time and impact your mortgage payments.

Competitive Fixed and Variable Rates

Flexible Payment Options

Generous Prepayment Privileges

Portability Options

Specialized Mortgage Programs

To apply for a TD mortgage, you’ll need the following:

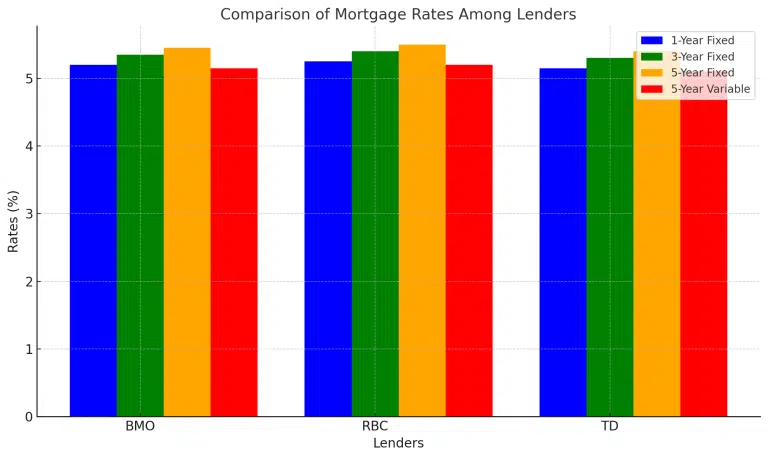

| Lender | 1-Year Fixed | 3-Year Fixed | 5-Year Fixed | 5-Year Variable |

|---|---|---|---|---|

| BMO | 5.20% | 5.35% | 5.45% | 5.15% |

| RBC | 5.25% | 5.40% | 5.50% | 5.20% |

| TD | 5.15% | 5.30% | 5.40% | 5.10% |

This table highlights how TD bank competes with other leading Canadian lenders, offering competitive rates and flexible terms.

Using a mortgage broker that has access to some of the lowest mortgage rates in Canada, is key to ensure you have the best approval rate.

| Feature | Fixed Rates | Variable Rates |

|---|---|---|

| Interest Rate Stability | Fixed throughout the term | Fluctuates with market rates |

| Payment Consistency | Predictable payments | Payments may vary |

| Risk Level | Low | Moderate to high |

| Ideal For | Long-term planners | Risk-tolerant borrowers |

Cashback Mortgages

Home Equity Line of Credit (HELOC)

First-Time Homebuyer Mortgages

Refinancing Options

To qualify for TD Bank’s best mortgage rates, you’ll need:

Good Credit Score

Stable Income

Sufficient Down Payment

Acceptable Debt-to-Income Ratio

TD Bank mortgage rates tend to sit in the mid-range of interest rates compared to other providers. For example, while TD’s five-year fixed rate was 5.44%, Bank of Nova Scotia was 6.43% and RBC was at 5.69%. On the lower end, BMO and CIBC were just above 5%, while HSBC was at 4.89%. So, it pays to shop around.

TD Mortgage online applications make it easy to apply for a mortgage. You’ll need the following information to complete the process:

A TD Mortgage Specialist will contact you within 24 hours to review your application and discuss the next steps of the application process. Of course, you can also set up an appointment at your local TD Bank to complete the process in person. However, it is always best to seek pre-approval first to know how much they are willing to lend you before you start your house hunt. Their online process offers an immediate response, and they hold your interest rate for 120 days upon pre-approval.

Although Canadian lenders post their mortgage rates, you can try to negotiate a better rate. Mortgage lenders are highly competitive, and depending on current market conditions, your employee status, and your credit score, they might be willing to give you a bit of a break.

The terms of your mortgage agreement determine prepayment charges as follows:

As a new Canadian without an established credit history, you can still qualify for a TD mortgage if you are or have applied to become a permanent resident and have been in Canada for five years or less.

Pros

Cons

The TD Bank started off as the Bank of Toronto in 1855, founded by a group of millers and merchants. In 1871 the first branch of the Dominion Bank opened, and the two banks merged in 1955, forming Toronto Dominion Bank. In 2000, TD acquired Canada Trust and then entered the U.S. retail banking arena when it acquired Banknorth in 2005.

While 33% of non-homeowners believe they’ll never own*, our Citadel mortgage brokers are 100% confident they can make it happen. How? With our expert advice and guidance.

(5-years interest savings with Citadel Mortgages)**

(Interest savings with Citadel Mortgages)

(5-years interest savings with Citadel Mortgages)**

(Interest savings with Citadel Mortgages)

Citadel Mortgages operates an information-based website that displays mortgage rates from its partners. While the company strives to provide the best possible rates, it cannot guarantee their accuracy at all times. Therefore, Citadel Mortgages accepts no liability for the precision of the information presented and is not accountable for any damages resulting from its use. Terms and conditions apply, and it is necessary to speak with a mortgage broker for further details. Please note that the rates displayed in this article are for article use only.

TD Bank offers some of the most competitive mortgage products in Canada, with flexible terms and exclusive features like cashback mortgages and HELOCs.

At Citadel Mortgages, we specialize in helping Canadians navigate the complexities of mortgage rates and terms. Whether you’re looking for a 6-month fixed rate, a 5-year variable, or something in between, our team is here to provide personalized guidance and access to the best rates in Canada.

See how you can save and become mortgage-free sooner

Calculate how much you’d spend each month to buy a home or renew or refinance your mortgage.

Discover how much cash back you could receive with our Cash Back Mortgage Calculator.