Today’s Mortgage Rates updated as of July 28, 2026 2:55 pm

5-year fixed*

5-year Variable*

*Insured loans. Other conditions apply. Rate in effect as of today.

Scotiabank, one of Canada’s leading financial institutions, offers a wide range of mortgage products tailored to fit the unique needs of Canadian homeowners. Whether you’re buying a new home, refinancing, or investing in real estate, Scotiabank provides flexible options and competitive rates.

At Citadel Mortgages, we ensure you access the best Scotiabank mortgage rates while simplifying the process for a seamless experience.

Whether you’re a first-time homebuyer, refinancing, or renewing your mortgage, understanding current trends and available options helps you make informed financial decisions.

This guide focuses on helping you navigate the Canadian mortgage market, offering insights into current rates, strategies for securing the best deal, and regional trends.

Mortgage brokers play a pivotal role in helping Canadians find tailored financing options, providing expert advice, and navigating the often complex mortgage market.

For more detailed information on mortgage types, costs, and rights, consult the Government of Canada – Financial Consumer Agency of Canada (FCAC).

Compare ScotiaBanks’s rates to other top lenders to ensure you’re getting the best deal. Contact us to explore all your options.

Learn more about today’s best mortgage rates in Canada.

Prime Rate | Variable Rates | Fixed Rates | Per Term Rates | Rate History | Pre-approval | Checklist | Features | How To | Pros & Cons | FAQ

Scotiabank’s prime rate aligns with the other Big Six banks. Scotiabank uses the prime rate to guide its decisions on its loan and mortgage rates. As well the prime rate also determines the interest rate for its variable mortgages, which rises and falls with the prime.

The variable mortgage rates are based on Scotiabank’s Prime Rate. The mortgage rate won’t go above the cap rate, which is the highest interest rate the bank will charge you. It’s important to understand the cap rate for variable mortgages. Despite being impacted by fluctuating interest rates, you still pay a fixed payment based on the cap rate. This payment doesn’t change. Instead, the changing interest rates impact how much of your payment goes toward the principal. The lower the interest rate, the more of your payment goes to your principal.

Scotiabank fixed mortgage rates have a set interest rate and mortgage payment for the full term of your mortgage. So, if you have a 5-year fixed-rate mortgage, you pay the same monthly payment for five years. However, once that term ends, your mortgage is up for renewal. At that time, your interest rates change based on current Scotiabank interest rates, which then impacts your monthly payments.

| Feature | Fixed Rate Mortgages | Variable Rate Mortgages |

|---|---|---|

| Interest Rate | Fixed throughout the term | Adjusts with market conditions |

| Payment Stability | Predictable | May fluctuate over time |

| Risk Level | Low | Moderate to high |

| Ideal For | Long-term stability seekers | Risk-tolerant individuals |

Here is a brief history of Scotiabank mortgage rates over the past three years:

Scotiabank’s eHome app allows you to get an online exclusive rate guarantee and download a letter of pre-approval in a matter of minutes. Pre-approval should be the first step you take when buying a home, as it tells you:

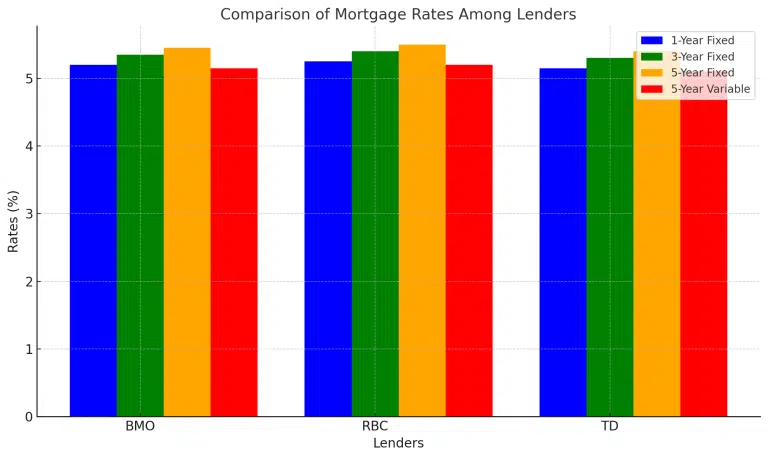

| Lender | 1-Year Fixed | 3-Year Fixed | 5-Year Fixed | 5-Year Variable |

|---|---|---|---|---|

| BMO | 5.20% | 5.35% | 5.45% | 5.15% |

| RBC | 5.25% | 5.40% | 5.50% | 5.20% |

| TD | 5.15% | 5.30% | 5.40% | 5.10% |

This table highlights how ScotiaBank competes with other leading Canadian lenders, offering competitive rates and flexible terms.

Using a mortgage broker that has access to some of the lowest mortgage rates in Canada, is key to ensure you have the best approval rate.

Before applying for a Scotiabank mortgage, you’ll need the following documents:

Self-employed individuals require one of the following for proof of income:

Most banks offer similar features focused on helping you pay down your mortgage faster, reducing interest or, in some cases, even missing a payment each year. Scotiabank offers the following mortgage features:

Cashback Mortgages

Prepayment Options

STEP Program (Scotiabank Total Equity Plan)

As mentioned above, Scotiabank does not advertise its best mortgage rates. Therefore, you want to ask if they can do better. Keep in mind banks tend to reserve their best rates for clients with an exceptional credit history, but it never hurts to ask. In this case, it’s best to set up an appointment with one of their Home Financing Advisors so that you can speak face-to-face with a representative. They will help you understand what the bank is willing to offer based on your specific financial situation.

The higher your credit score and the better your credit history, the more likely the advisor is to be willing to go to bat for you. Another strategy is to go prepared with research about interest rates so you can lay out all the comparable mortgages being offered by the competition. It never hurts to leverage your knowledge to show them you are willing to walk to get the best rate. Avoid sharing information about smaller lenders, as Big Six banks don’t feel obligated to compete with those lenders.

As mentioned above, Scotiabank does not advertise its best mortgage rates. Therefore, you want to ask if they can do better. Keep in mind banks tend

Before you decide on the bank you’d like to do business with, it’s important to consider the pros and cons of their mortgage products. Here are the pros and cons of Scotiabank mortgages:

Pros

Cons

Rates can change based on the Bank of Canada’s interest rate announcements and market conditions.

Scotiabank makes it easy to apply for a mortgage with the following three options to suit your needs:

Yes. You can always try to negotiate a better mortgage rate. Because Scotiabank’s interest rates are the highest out there, you might stand a chance of them offering a lower rate if you show them what other banks offer. Also, as mentioned, they tend not to advertise their best rates, so it’s worth asking if they can do better.

Yes, Scotiabank’s cashback program provides up to 5% cashback, which can be used for renovations, moving costs, or other needs.

Yes, Scotiabank offers a seamless mortgage switch program with competitive rates and flexible options.

Several factors impact the rates offered by ScotiaBank, including:

We compare mortgage rates from top lenders, including BMO mortgage rates, CIBC mortgage rates, RBC mortgage rates, TD Bank Mortgage Rates, and MCAP mortgage rates, alongside our exclusive Citadel Smart Home Plan mortgage rates. Let us simplify the process and help you secure approval quickly and stress-free!

While 33% of non-homeowners believe they’ll never own*, our Citadel mortgage brokers are 100% confident they can make it happen. How? With our expert advice and guidance.

(5-years interest savings with Citadel Mortgages)**

(Interest savings with Citadel Mortgages)

(5-years interest savings with Citadel Mortgages)**

(Interest savings with Citadel Mortgages)

Scotiabank offers a wide range of mortgage solutions designed to meet the needs of Canadian homeowners. With competitive rates, flexible terms, and innovative programs like STEP, Scotiabank is an excellent choice for your mortgage. Partner with Citadel Mortgages to access the best rates and enjoy a seamless experience tailored to your needs.

At Citadel Mortgages, we specialize in helping Canadians navigate the complexities of mortgage rates and terms. Whether you’re looking for a 6-month fixed rate, a 5-year variable, or something in between, our team is here to provide personalized guidance and access to the best rates in Canada.

See how you can save and become mortgage-free sooner

Calculate how much you’d spend each month to buy a home or renew or refinance your mortgage.

Discover how much cash back you could receive with our Cash Back Mortgage Calculator.