Today’s Mortgage Rates updated as of July 28, 2026 2:20 pm

5-year fixed*

5-year Variable*

*Insured loans. Other conditions apply. Rate in effect as of today.

As one of Canada’s largest and most trusted banks, RBC (Royal Bank of Canada) offers a variety of competitive mortgage options for homebuyers, refinancers, and investors. Whether you’re a first-time homebuyer, refinancing, or renewing your mortgage, understanding current trends and available options helps you make informed financial decisions.

This guide focuses on helping you navigate the Canadian mortgage market, offering insights into current rates, strategies for securing the best deal, and regional trends.

Mortgage brokers play a pivotal role in helping Canadians find tailored financing options, providing expert advice, and navigating the often complex mortgage market.

For more detailed information on mortgage types, costs, and rights, consult the Government of Canada – Financial Consumer Agency of Canada (FCAC).

Compare RBC mortgage rates to other top lenders to ensure you’re getting the best deal. Contact us to explore all your options.

Learn more about today’s best mortgage rates in Canada.

Prime Rate | Per Term Rates | Features | How To | Products | FAQ

RBC’s prime rate is used to calculate interest rates for their products, including their mortgage rates. The prime interest rate impacts variable bank rates, while fixed rates already in place are not affected. The current RBC Royal Bank prime rate aligns with the going prime rate of most major financial institutions in Canada.

RBC Royal Bank 5-Year Fixed and Variable Rate History

Over the past three years, the RBC’s rate history was as follows:

| Feature | Fixed Rate Mortgages | Variable Rate Mortgages |

|---|---|---|

| Interest Rate | Fixed throughout the term | Fluctuates with market conditions |

| Payment Stability | Predictable | May vary over time |

| Risk Level | Low | Moderate to high |

| Ideal For | Long-term stability seekers | Risk-tolerant individuals |

RBC offers extra features designed to suit your financial situation, whether you need to relieve financial stress or want to pay down your mortgage sooner without any penalties. These features include:

When buying a new home, you require the following documentation to support your mortgage request through the RBC:

If you currently own a home, you also need the following:

Other information:

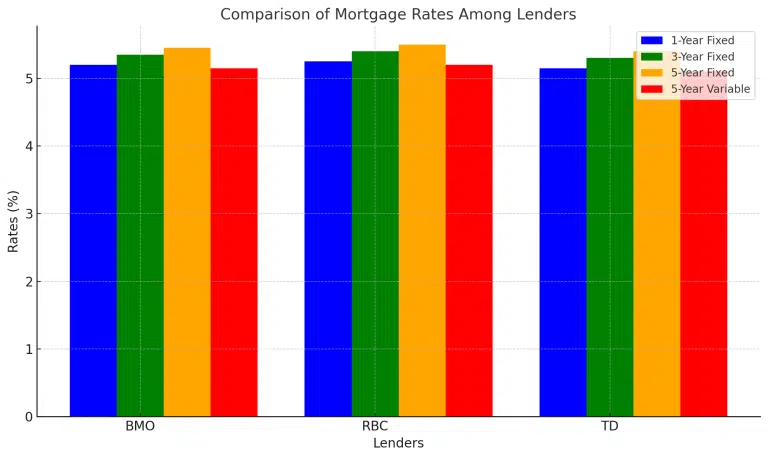

| Lender | 1-Year Fixed | 3-Year Fixed | 5-Year Fixed | 5-Year Variable |

|---|---|---|---|---|

| BMO | 5.20% | 5.35% | 5.45% | 5.15% |

| RBC | 5.25% | 5.40% | 5.50% | 5.20% |

| TD | 5.15% | 5.30% | 5.40% | 5.10% |

This table highlights how RBC competes with other leading Canadian lenders, offering competitive rates and flexible terms.

Using a mortgage broker that has access to some of the lowest mortgage rates in Canada, is key to ensure you have the best approval rate.

Competitive Interest Rates

Flexible Mortgage Options

Exclusive Programs

Trusted Name

To apply for an RBC mortgage, you can set up an appointment with your local RBC or use their online and over-the-phone options. You can use our RBC document checklist below to ensure you have all the information required for the application process. Also, it often works in your best interest to arrange an appointment with a mortgage specialist as you can discuss your needs and receive advice on the best mortgages for your needs.

A mortgage pre-approval is always best when buying a home. RBC will pre-approve your mortgage by first running a credit check and then setting a pre-approved rate they hold for you for 120 days. Should interest rates increase as you search for a home, the RBC honours the rate agreed upon at the time of pre-approval. However, if rates increase, the lower rate is honoured. You can apply either in person, online or over the phone.

This mortgage is used when buying an investment property or converting your home into a rental property. With this mortgage, RBC can offer up to 80% of your home’s appraised value.

If you are interested in buying a vacation or second home, this mortgage finances up to 95% of the appraised value. It depends on whether you already own a home and the purchase price of the second property.

The cashback mortgage provides up to 7% of your mortgage value in cash, to a maximum amount of $20,000. The amount is then added to your mortgage amount, which you pay back as part of your mortgage balance.

If you are self-employed, a freelancer or own your own business, this is the mortgage for you. The RBC self-employed mortgage allows you to finance up to 80% of the appraised value of your home when you are refinancing and up to 90% when you are purchasing a home.

If you are seeking a property in the U.S., the RBC has branches in states such as Georgia, Florida and North Carolina. This makes it easier to get a mortgage if you don’t have a U.S. credit history. As a Canadian bank, RBC leverages your Canadian credit history and your Canadian assets, so you can purchase a U.S. home.

This easy lending solution combines your traditional mortgage with a HELOC (RBC Royal Credit Line®), allowing you to leverage lower fixed interest rates to protect against possible future interest rate fluctuations. You also have the choice to divide your mortgage into fixed-rate and variable-rate portions if you prefer.

Several factors impact the rates offered by RBC, including:

We compare mortgage rates from top lenders, including BMO mortgage rates, CIBC mortgage rates, RBC mortgage rates, TD Bank Mortgage Rates, and MCAP mortgage rates, alongside our exclusive Citadel Smart Home Plan mortgage rates. Let us simplify the process and help you secure approval quickly and stress-free!

No, they tend to be in the mid-range. For example, while RBCs’ 5-year fixed rate is 5.69%, TD’s is 5.44%, BMO’s is 5.09% and CIBC’s is 6.49%. So it pays to shop around when looking for the lowest rate.

You can apply for a mortgage by either setting up an appointment with a mortgage specialist at the bank, filling out a form online, or doing it over the phone.

Yes, you do have a right to negotiate your rate. However, RBC is tougher than other banks, and you are less likely to see them bend on their mortgage rates. That said, with fewer home buyers in the market of late, they might be willing to negotiate to get your business.

The RBC honours their quoted fixed-rate mortgages for up to 120 days and will reduce the rate should a better rate be available at the time you buy your home.

While 33% of non-homeowners believe they’ll never own*, our Citadel mortgage brokers are 100% confident they can make it happen. How? With our expert advice and guidance.

(5-years interest savings with Citadel Mortgages)**

(Interest savings with Citadel Mortgages)

(5-years interest savings with Citadel Mortgages)**

(Interest savings with Citadel Mortgages)

RBC offers a variety of mortgage products that cater to every homeowner’s needs. With Citadel Mortgages, you can access the best RBC rates and programs while benefiting from personalized advice and tailored solutions.

At Citadel Mortgages, we specialize in helping Canadians navigate the complexities of mortgage rates and terms. Whether you’re looking for a 6-month fixed rate, a 5-year variable, or something in between, our team is here to provide personalized guidance and access to the best rates in Canada.

See how you can save and become mortgage-free sooner

Calculate how much you’d spend each month to buy a home or renew or refinance your mortgage.

Discover how much cash back you could receive with our Cash Back Mortgage Calculator.