Today’s Home Equity Loan Rates updated as of July 28, 2026 3:31 pm

Home Equity Loan Rates Start From*

*Home equity loan rates range from 4.99-16.99 with the average rate being 10.99%. Home equity loans carry lender and brokerage fees that range from 2-10% with the average being 6%. Other conditions apply. Rate in effect as of today.

Home equity loans are a secured loan that allows homeowners to tap into the equity they’ve built in their property, providing access to additional funds without altering their existing mortgage. This financial tool is particularly popular among Canadians who want to utilize their home equity for various purposes, such as home improvements, debt consolidation, or significant life events.

When you take out a home equity loan, you’re adding an additional loan to a property that already has a mortgage. This is inherently riskier for lenders because they hold a secondary claim on the property’s title. In the event of a default, the lender in the first position is prioritized for repayment from the property sale proceeds. Consequently, the lender in the second position faces a higher risk of not being fully repaid, which is why interest rates for home equity loans are typically higher than those for primary mortgages.

For homeowners with a good credit score and more than 20% home equity, the most cost-effective option for a home equity loan is often a home equity line of credit (HELOC). A HELOC functions as a revolving line of credit, allowing you to borrow against your home’s equity as needed, much like a credit card. On the other hand, for those with weaker credit or less equity, a traditional home equity loan obtained through a trust company or private lender may be necessary.

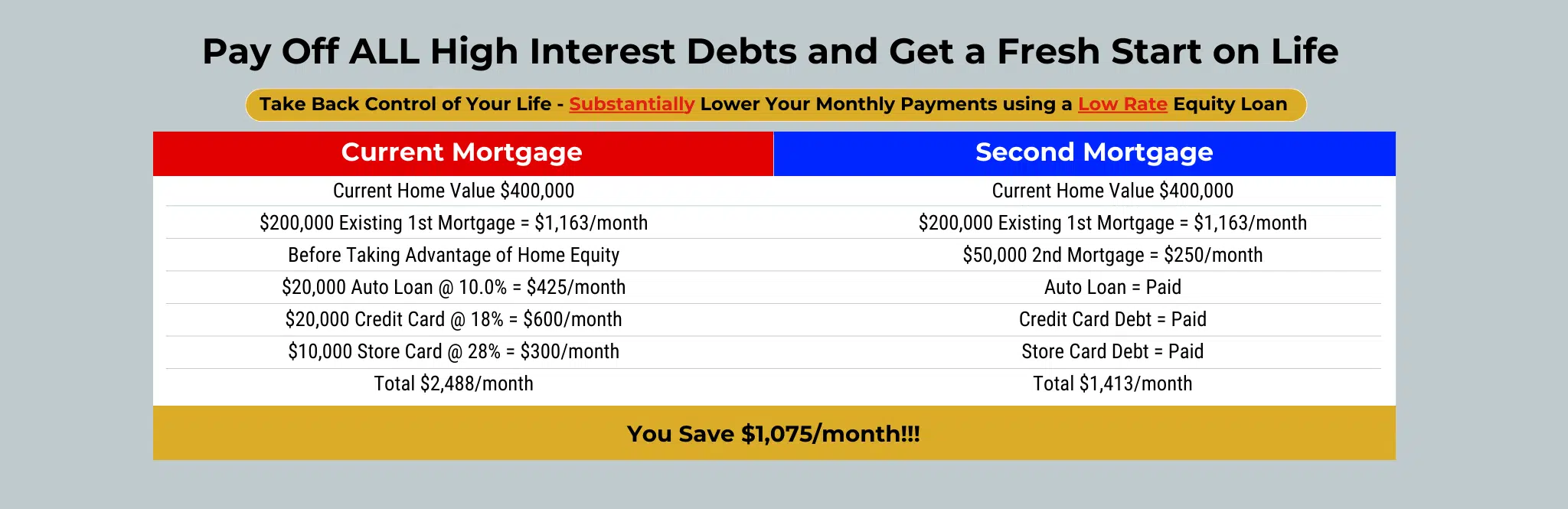

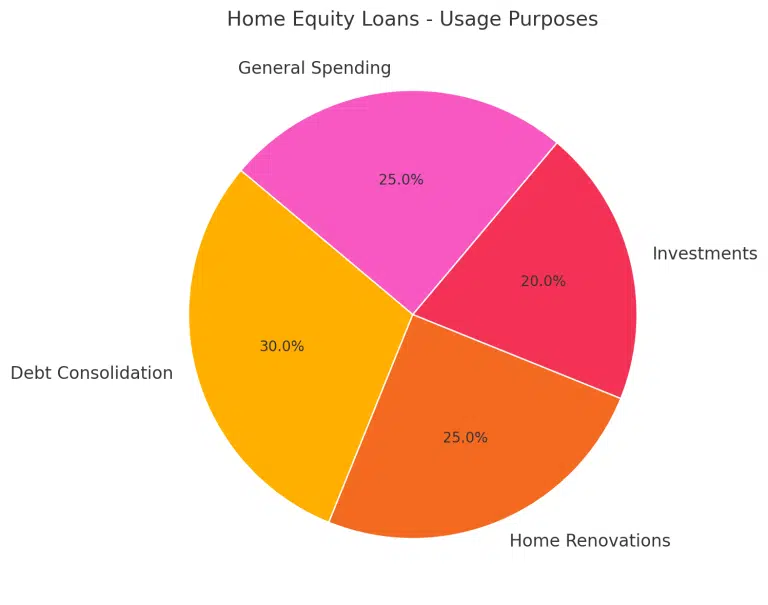

You can use home equity loans for anything. However, homeowners usually access the money for the following:

You can borrow up to 80% of your home’s current market value, less what you still owe on your primary mortgage. If your home is worth $800,000, the calculation would be $800,000 x 0.80 = $640,000. However, you then have to deduct the amount owed. So, if you still owe $200,000, you would have to remove that from the $640,000, leaving you up to $440,000 the lender might be willing to loan you. Some private mortgage lenders allow up to 95% of your home value but at much higher rates and fees.

There are many advantages of a home equity loan, including:

You also have to consider the disadvantages of a home equity loan, such as:

| Program Name | Mortgage Amount | Loan to Value | Total Debt Servicing | Credit Minimum | Bankruptcy/Consumer Proposal | Term | Amortization | Pre-payment Penalty | Funding Time | Interest Rates | Closing Cost Fees | Lender Fees | Brokerage Fees |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| HELOC in 2nd Position – Bank Product | Up to $500,000 | Up to 75% (80% in main cities) | 39/44 or 46/50 | 680 or higher | No bankruptcy/consumer proposal in past 7 years and 2 active trade lines | HELOC Open | None – Interest Only Payments | Open to pay off anytime | 2-4 weeks once approved | Bank of Canada + 0.50-2% | $600-$1500 | None | None |

| HELOC in 2nd Position – Non-Bank Product | Up to $500,000 | Up to 75% (80% in main cities) | 48/48, 50/50, or 60/60 (depending on LTV and location) | No minimum | Can be in bankruptcy/consumer proposal but must be paid out if approved | HELOC Open | None – Interest Only Payments | Open to pay off anytime | 2-4 weeks once approved | Bank of Canada + 2-3% | $600-$1500 | 1%-4% | 1%-4% |

| HELOC in 2nd Position – Private Mortgage | Up to $500,000 | Up to 75% (80% in main cities) | Common sense lending (depending on LTV and location) | No minimum | Can be in bankruptcy/consumer proposal but must be paid out if approved | HELOC Open | None – Interest Only Payments | Open to pay off anytime | 24-72 hours once approved | 10.99%-17.99% | $3500 | 2%-4% | 2%-4% |

Disclaimer: All the above costs, terms, and interest rates are estimates and are subject to the strength of the application, the property's location, and On Approved Credit (OAC). Actual terms may vary. This information is provided for informational purposes only and does not constitute financial or legal advice. Citadel Mortgages is not liable for any decisions made based on this information. For exact details, please contact us directly.

| Program Name | Mortgage Amount | Loan to Value | Total Debt Servicing | Credit Minimum | Bankruptcy/Consumer Proposal | Term | Amortization | Pre-payment Penalty | Funding Time | Interest Rates | Closing Cost Fees | Lender Fees | Brokerage Fees |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Home Owners Secured Loan | $5,000 - $60K | Up to 100% | Up to 75% | 500 | Discharged for 4+ years | 36 to 120 months | 10 Years | 6 months interest if paid off before 36 months | 24-72 hours | 19.99%-24.49% | $600-$900 | None | None |

| Home Owners Express Second Mortgages | Up to $125K | Up to 80% | Up to 75% | 500 | Discharged for 4+ years | 1-5 Years | 20 Years | 6 months interest if paid off before 36 months | 24-72 hours | Starting at 17.90% | $600-$900 | None | None |

| Home Owners Low Rate Express Second Mortgage | Up to $200K | Up to 75% | Up to 75% | 600 | Discharged for 3+ years | 6-36 months | 120-240 months | Open to pay off anytime | 24-72 hours | 4.99%-11.99% | $600-$900 | 3%-8% | None |

| Home Owners Normal Second Mortgage | Up to $1M | Up to 75% (80% in main cities) | Common Sense Lending | No Minimum | Can be in or paying off one | 12 months | None - Interest Only Payments | Depends on mortgage | 24-72 hours | 10.99%-15.99% | $3500 | 3%-8% | 3%-8% |

Disclaimer: All the above costs, terms, and interest rates are estimates and are subject to the strength of the application, the property's location, and On Approved Credit (OAC). Actual terms may vary. This information is provided for informational purposes only and does not constitute financial or legal advice. Citadel Mortgages is not liable for any decisions made based on this information. Home Owners Low Rate Exprres Second Mortgage only in Ontario. For exact details, please contact us directly.

Applying for a home equity loan involves several vital steps to secure the best terms and rates. Here’s a comprehensive guide to help you through the process:

At Citadel Mortgages, we are committed to simplifying the home equity loan application process. Our experienced mortgage agents will guide you through each step, ensuring you get the best possible terms and rates tailored to your financial needs. We understand that applying for a home equity loan can be a complex process, and we are here to make it as straightforward as possible for you. With our expertise and personalized service, you can navigate the process with confidence.

At Citadel Mortgages, we understand that there are times when you need a home equity loan. Our tailored Home Equity program allows you to access up to 95% of your home equity, even if you have bad credit or low income. . If you have a history of bankruptcy or are currently in a consumer proposal, then you can access up to 80% of your home equity.

Our home equity loan program offers several advantages:

A home equity loan is an additional mortgage loan against the equity in your home that already has a mortgage. For lenders, this is riskier than the first mortgage because they are second in line to be paid if the homeowner defaults. As a result, home equity loans rates are typically higher than first mortgage rates.

Even if you have bad credit or low income, Citadel Mortgages can help. Our expert team specializes in fast home equity loans, ensuring that as long as your home has equity, you can get the approval you need.

Applying for a home equity loan with Citadel Mortgages is simple and straightforward. Here’s how:

When considering a home equity loan, it’s not just about the money you’ll receive, but also about the fees you’ll encounter. Understanding these costs upfront is a powerful tool that puts you in control, helping you evaluate whether the benefits outweigh the expenses. Here are some standard fees you may encounter:

Mortgage agents typically charge a brokerage fee because lenders do not compensate them for the time spent on your file. This fee is generally equivalent to the lender’s fee and covers the mortgage agent’s efforts in managing and processing your mortgage application.

Understanding all the fees associated with a home equity loan is essential for making an informed decision about pursuing one. By evaluating the costs and benefits, you can determine if a home equity loan is right for you.

Typically, all fees are included in your mortgage amount, so you do not have to pay them out of pocket. However, if there is insufficient equity in your home or if it is a purchase transaction, you will need to pay these fees separately rather than add them to the mortgage.

At Citadel Mortgages, we provide clear information on all potential fees to ensure you are fully informed. Our goal is to inform you and guide you through the complexities of securing a home equity loan, providing the support you need to make the right decisions.

Having bad credit doesn’t automatically disqualify you from getting a home equity loan. While traditional lenders may be hesitant, options are still available through private lenders and specialized mortgage programs. Here’s what you need to know:

Home equity loan payments are typically structured around interest-only payments, with most lenders offering a monthly payment schedule. However, at Citadel Mortgages, we offer flexible payment options to suit your financial needs.

To ensure a smooth and efficient home equity loan closing process for please prepare the following documents:

Using a home equity loan calculator can help you determine the potential costs and benefits of taking out a home equity loan. At Citadel Mortgages, we provide a comprehensive home equity loan calculator designed to give you accurate insights into your borrowing potential and monthly payments.

The home equity loan calculator will then produce an estimate for you, please be sure to contact one of our mortgage brokers at Citadel Mortgages to help you get approved today!

Here is an overview of each:

Home equity loans

HELOC

When you apply for a home equity loan, the lender will perform a hard credit check to evaluate your credit score and assess your creditworthiness. Your credit score and credit history play a crucial role in determining the interest rate for your home equity loan. Be mindful that multiple credit inquiries from different lenders can negatively impact your credit score.

For personalized advice on securing a home equity loan and understanding the impact on your credit, reach out to Citadel Mortgages. Our experts are here to guide you through the process and help you find the best terms.

It depends on the lender. The best home equity loan rates in Canada are HELOCS, followed by home equity loans and then private loans.

Home equity loans can close in as little as 48-72 hours as long as our clients provide all required documents upfront. With that said, typically, processing and approving a home equity loan can take at least 30 days to close. Really at the end of the day you can control how fast this can close by ensuring you provide everything we need upfront.

You can get a home equity loan with bad credit by paying higher interest rates or having someone co-sign the loan. You can also consider a private lender, but will have to pay more than double the interest rates in most cases.

Even if you are up to date on your first mortgage payments, the lender can start foreclosure proceedings to take your home if you fail to make payments on your home equity loan.

Yes sometimes you can pay off your home equity loan early, other times you might not be able too, this comes down to the details of your terms on your home equity loan and is important to review.

While a home equity loan can provide a way to pay off high-interest debts or fund significant renovation projects, it might not always be the best financial decision. You may have more affordable alternatives if you have substantial home equity or a good credit score.

Conclusion

Before opting for a home equity loan, exploring all your financial options is crucial. This way, you can be reassured that you’re choosing the most affordable and beneficial solution for your needs.

A second mortgage in Canada is usually a 1 year interest only term.

Understanding the landscape of home equity loans in Canada can help you make informed decisions. Here are some key statistics:

This information is based on the most up-to-date statistics available, sourced from various reliable resources, including Canada’s National Statistics Agency. While we strive to keep our data current, these figures may change as new information becomes available.

Obtaining a home equity loan has its advantages and disadvantages. Home equity loans offer the opportunity to access the equity in your home for purposes like consolidating debt, making home improvements, or funding the down payment on a second home.

It’s important to note that a home equity loan represents a significant financial commitment in addition to your existing payments, which can impact your debt-to-income ratios. Home equity loans typically carry higher interest rates compared to your first mortgage, as lenders must account for the increased risk of being in a secondary position. Contact the experts at Citadel Mortgages for personalized advice to determine if a home equity loan is suitable for your situation!

For tailored guidance and competitive rates, get in touch with Citadel Mortgages. Our team will assist you throughout the process and support you in making sound financial decisions.

At Citadel Mortgages, we pride ourselves on offering expert, client-focused mortgage solutions that stand out in the industry. Here’s why you should choose us:

Our mortgage brokers are licensed and certified across multiple provinces, providing exceptional advice and service tailored to your unique needs. Our mortgage brokers are committed to delivering the highest standards of professionalism and expertise.

Unlike traditional commission-based models, our mortgage agents are evaluated based on client satisfaction and the quality of their advice. This ensures that you receive impartial guidance on the best mortgage options for your situation.

Citadel Mortgages offers competitive rates that help you save money over the life of your mortgage. Our team works diligently to find the most favorable terms to suit your financial goals.

We are dedicated to transforming the mortgage industry by offering a transparent, seamless process. Our 100% digital platform ensures that you can manage your mortgage application from start to finish with ease and confidence.

At Citadel Mortgages, our mission is to provide a positive, empowering, and transparent property financing experience. We simplify the mortgage process to make it as straightforward and stress-free as possible.

For personalized advice and the best mortgage rates in Canada, contact our licensed and knowledgeable mortgage experts at Citadel Mortgages.