Today’s Reverse Mortgage Rates updated as of July 17, 2026 7:47 pm

*Rates can change at anytime. Other conditions apply. Rate in effect as of today.

Reverse mortgage rates in Canada vary depending on factors such as your home’s value, location, and the chosen lender. This guide will provide a detailed overview of current reverse mortgage rates, factors influencing those rates, and tips to secure the best deal.

We’ll also give you a detailed breakdown of the latest rates from leading providers, including HomeEquity Bank, CHIP Reverse Mortgage, Bloom Reverse Mortgage, and Equitable Bank Reverse Mortgage.

Reverse mortgage rates are the interest rates applied to funds borrowed against your home’s equity. Unlike traditional mortgages, reverse mortgages allow homeowners aged 55+ to access their home equity without the need for monthly repayments. The loan is repaid when the home is sold or the homeowner moves out permanently.

For more details on how reverse mortgages work, visit the Financial Consumer Agency of Canada (FCAC).

Type of Rate:

Loan-to-Value Ratio (LTV):

The percentage of your home’s value that you can borrow. Higher LTVs may lead to slightly higher rates.

Home Value and Location:

Urban areas often qualify for better rates due to higher property values and demand.

Market Conditions:

Economic factors such as the Bank of Canada’s interest rate policy influence reverse mortgage rates.

To qualify, you must meet the following criteria:

For more information on eligibility, visit CMHC’s Reverse Mortgage Guide.

| Lender | Fixed Rates | Variable Rates | Administrative Fees |

|---|---|---|---|

| HomeEquity Bank | 7.00% – 8.95% | 6.65% – 8.50% | $1,795 |

| Equitable Bank | 7.25% – 9.10% | 6.90% – 8.75% | $995 |

| Bloom Financial | 6.95% – 9.00% | 6.75% – 8.80% | $1,495 |

Reverse mortgages offer a great way for Canadian homeowners aged 55 and older to access the equity in their homes. Below is a comparison of reverse mortgage options from two leading lenders in Canada: HomeEquity Bank and Equitable Bank. Bloom is another reverse mortgage lender option as well here in Canada.

Rates Overview:

Why Choose HomeEquity Bank?

HomeEquity Bank offers the well-established CHIP Reverse Mortgage, allowing homeowners in Winnipeg to access up to 55% of their home’s equity. One of the standout features is the no-negative-equity guarantee, which ensures that you will never owe more than the value of your home when it’s sold. This provides peace of mind while offering financial flexibility to meet your needs.

Learn more about their offerings at HomeEquity Bank.

Rates Overview:

Why Choose Equitable Bank?

Equitable Bank offers some of the most competitive rates in the reverse mortgage market. With both fixed and variable rate options, homeowners in Winnipeg can choose a plan that aligns with their financial goals. Equitable Bank’s flexible loan structure allows borrowers to tailor their reverse mortgage for debt consolidation, home improvements, or supplementing retirement income.

For more details, visit Equitable Bank’s Reverse Mortgage Page.

Rates Overview:

Bloom Financial provides competitive reverse mortgage rates in Canada, offering both fixed and variable rate options. These flexible rates ensure that homeowners can choose a plan tailored to their financial goals.

Why Choose Bloom Financial?

Bloom Financial specializes in helping Canadian homeowners aged 55 and older access up to 55% of their home’s equity in tax-free cash. One of Bloom’s standout features is its no-negative-equity guarantee, which ensures that you’ll never owe more than the fair market value of your home when it’s sold. This safeguard provides peace of mind and financial flexibility, allowing you to achieve your goals without the burden of monthly mortgage payments.

Learn more about Bloom Financial’s reverse mortgage solutions at Bloom Reverse Mortgage Page.

Both HomeEquity Bank and Equitable Bank offer reverse mortgages designed to help Canadian homeowners tap into their home equity safely and effectively. Comparing their rates and features allows you to make an informed decision tailored to your financial situation.

Compare Multiple Lenders

Evaluate rates from providers such as HomeEquity Bank, Equitable Bank, and Bloom to find the best deal.

Work with a Mortgage Broker

A broker can help negotiate competitive rates and terms tailored to your needs.

Consider Rate Lock Options

Locking in a rate during the application process can protect you from potential increases.

Maintain a Low LTV

Borrowing a smaller percentage of your home’s equity can lead to more favorable rates.

Understanding the market trends and usage patterns for reverse mortgages can help you make informed decisions. Here are key statistics:

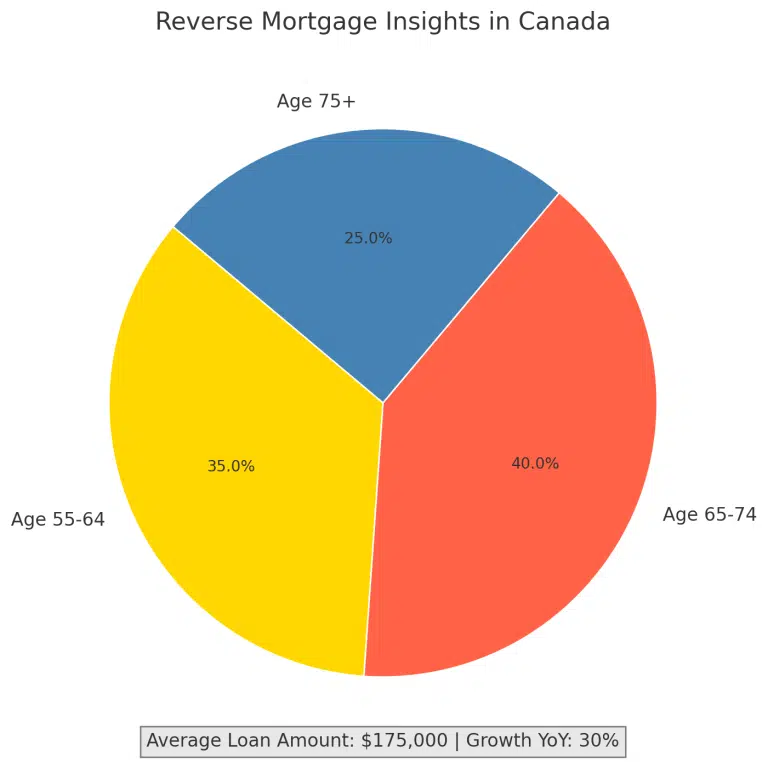

Reverse mortgages have become an increasingly popular financial tool among Canadian homeowners aged 55 and older, allowing them to access the equity in their homes without selling the property. Below are key statistical insights into the reverse mortgage landscape in Canada:

Market Growth and Size

Outstanding Reverse Mortgage Debt: As of 2022, the total outstanding reverse mortgage debt in Canada surpassed $6 billion, reflecting a significant increase in demand for this financial product.

Annual Growth Rate: HomeEquity Bank, a leading provider of reverse mortgages in Canada, reported a 30% increase in demand for its CHIP Reverse Mortgage product in 2022 compared to the previous year.

Demographic Trends

Loan Characteristics

Average Reverse Mortgage Amount: The average reverse mortgage amount in Canada is approximately $175,000.

Loan-to-Value (LTV) Ratios: Canadian homeowners can typically access up to 55% of their home’s appraised value through a reverse mortgage, depending on factors such as age, property value, and location.

Interest Rates: Reverse mortgage interest rates in Canada are generally higher than traditional mortgage rates, often ranging between 6.59% and 7.29% for fixed terms as of late August 2024.

Usage of Funds

Regional Insights

Lender Landscape

These statistics highlight the growing significance of reverse mortgages in Canada’s financial landscape, offering seniors a viable option to access their home equity and enhance their financial well-being during retirement.

Reverse mortgages provide financial flexibility, but it’s crucial to understand the associated costs. Below is a breakdown of typical fees and costs from leading Canadian reverse mortgage providers.

Interest Rates

Appraisal Fee

Legal Fees

Administrative Fees

Prepayment Penalties

The CHIP Reverse Mortgage could be what you need. It’s a sensible and straightforward way to unlock the value in your home and turn it into cash to enjoy life on your terms.

Yes, reverse mortgage rates are typically higher because they involve more risk for the lender. However, they offer unique benefits, such as no monthly payments.

Yes, variable rates fluctuate with the market, while fixed rates remain constant for the loan term.

It depends on your financial goals. Fixed rates offer predictability, while variable rates can provide savings if market rates drop.

No, both you and your spouse must be at least 55 years old to qualify for a reverse mortgage in Canada.

No, as long as you meet your obligations, such as keeping your property taxes and insurance up to date, you can stay in your home for life.

Canadian reverse mortgages come with a no negative equity guarantee, meaning you’ll never owe more than the value of your home.

The loan is typically repaid when you sell your home, move into long-term care, or pass away.

You receive the money from the reverse mortgage tax-free. It is not added to your taxable income, so it doesn’t affect Old Age Security (OAS) or Guaranteed Income Supplement (GIS) government benefits you may receive.

What is a reverse mortgage, and how does it work?

It is a loan secured against the value of your home, but unlike a traditional Home Equity Line of Credit (HELOC) or a second mortgage, you are not required to make monthly mortgage payments for as long as you keep living in your home. You always maintain ownership and control of your home.

At Citadel Mortgages, we work with Canada’s top lenders to provide you with competitive reverse mortgage rates and personalized service. Here’s what we offer:

Understanding your reverse mortgage potential is easier with our Reverse Mortgage Calculator. This tool provides an instant estimate of how much equity you can access based on:

Try the Citadel Mortgages Reverse Mortgage Calculator today to explore your options!

Reverse mortgages offer a unique way for Canadian seniors to access their home equity without selling their property. By comparing rates and understanding the factors that influence them, you can make an informed decision that supports your financial goals. Contact Citadel Mortgages today to explore your options and secure the best reverse mortgage rate.