Today’s Mortgage Rates updated as of October 13, 2025 10:42 am

5-year fixed*

5-year Variable*

*Insured loans. Other conditions apply. Rate in effect as of today.

CIBC (Canadian Imperial Bank of Commerce) is one of the country’s leading lenders, offering competitive mortgage rates for fixed, variable, and cashback options. At Citadel Mortgages, we work to match you with the best mortgage solution from CIBC or other top lenders, ensuring you save money and achieve your financial goals.

Whether you’re a first-time homebuyer, refinancing, or renewing your mortgage, understanding current trends and available options helps you make informed financial decisions.

This guide focuses on helping you navigate the Canadian mortgage market, offering insights into current rates, strategies for securing the best deal, and regional trends.

Mortgage brokers play a pivotal role in helping Canadians find tailored financing options, providing expert advice, and navigating the often complex mortgage market.

For more detailed information on mortgage types, costs, and rights, consult the Government of Canada – Financial Consumer Agency of Canada (FCAC).

Compare CIBC mortgage rates to other top lenders to ensure you’re getting the best deal. Contact us to explore all your options.

Learn more about today’s best mortgage rates in Canada.

Prime Rate | Variable Rate | Fixed Rate | Per Term | Rate History | Checklist | Features | How it Works | How To | History | FAQ

CIBC’s Prime Rate provides the basis for their various loans and mortgages. Prime rates change when the Bank of Canada raises or lowers its overnight rate. The CIBC bases their mortgages on the prime rate, but because your home is collateral for the loan, the rate tends to be lower than the prime. However, we should point out that CIBC mortgage rates are closer to the prime than other leading Canadian banks.

If you have a variable-rate mortgage, your interest rate changes based on the specified financial index in your mortgage. This is often the CIBC Prime Rate. Your mortgage agreement explains how changing interest rates impact your payments. Often, your regular payments stay the same. However, when interest rates decrease, more of your payment covers the principal, while more goes towards interest if they increase.

If you have a fixed-rate mortgage, your interest rate and monthly payments stay the same for the full term of the mortgage agreement. However, once the term ends, the latest interest rates apply, changing how much you pay each month.

Here is a brief history of the past fixed and variable rates for CIBC:

CIBC offers some of the best fixed and variable rates, helping you secure lower monthly payments.

Pay up to 20% of your mortgage balance annually without penalties, reducing your interest costs.

Lock in your rate for up to 120 days, protecting you from rate increases while you shop for your home.

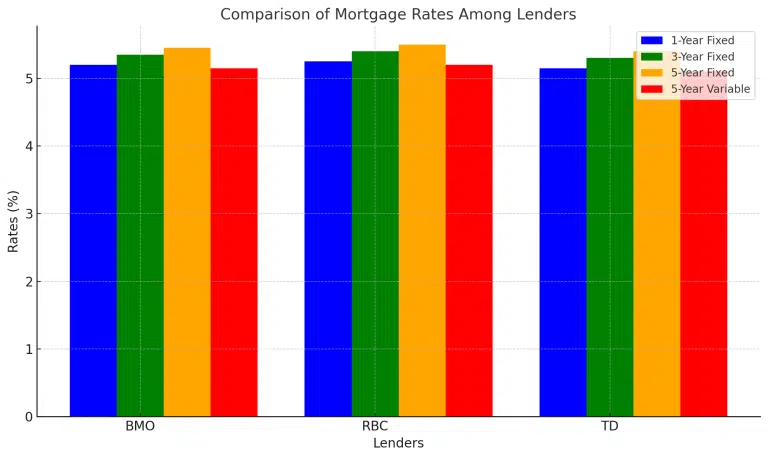

| Lender | 1-Year Fixed | 3-Year Fixed | 5-Year Fixed | 5-Year Variable |

|---|---|---|---|---|

| CIBC | 5.20% | 5.35% | 5.50% | 5.10% |

| RBC | 5.25% | 5.40% | 5.45% | 5.15% |

| TD | 5.15% | 5.30% | 5.40% | 5.05% |

By working with Citadel Mortgages, you can compare rates from CIBC and other lenders to ensure you get the best deal.

This table highlights how BMO competes with other leading Canadian lenders, offering competitive rates and flexible terms.

Using a mortgage broker that has access to some of the lowest mortgage rates in Canada, is key to ensure you have the best approval rate.

When applying for a CIBC mortgage, they require the following documents:

CIBC is often criticized for not offering any payment breaks for its clients like other leading banks in Canada. And this really is a big deal. Most banks offer an annual missed payment option each year. However, they do provide the following other features:

Mortgages are loans used specifically to purchase a home. As you pay down the loan, you build equity in your home. The equity is realized when you either sell your home or want to access cash via a home equity loan. Equity is the difference between what you owe on your mortgage and the value of your home.

Your mortgage has a “term” that determines how long the interest rates and conditions are in effect. This is usually five years but can be as short as a year or as long as 10. Each term comes with an interest rate, payment amount, and timeline, which are renegotiated and renewed when the period ends. Interest rates are based on CIBC’s current rates, which will impact how much your payments are each month.

The term is different from amortization. Amortization is the time it takes you to pay off your entire mortgage and all the interest the bank applies. It usually takes about 25 years to pay down a mortgage when you aren’t making any prepayments.

If you fail to make your payments over several months, the bank can “foreclose” on your mortgage and take your home to regain the money owed on the house.

Several factors impact the rates offered by CIBC, including:

We compare mortgage rates from top lenders, including BMO mortgage rates, CIBC mortgage rates, RBC mortgage rates, TD Bank Mortgage Rates, and MCAP mortgage rates, alongside our exclusive Citadel Smart Home Plan mortgage rates. Let us simplify the process and help you secure approval quickly and stress-free!

You can start the CIBC mortgage pre-approval process online. Complete their online application form, and someone will contact you. Pre-approval tells you whether you qualify for a CIBC mortgage or not. If you are eligible, CIBC tells you how much they will lend you. Pre-approval also provides a locked-in interest rate until you either find your home or for 120 days, whichever comes first. Should interest rates decrease, you will be given the lowest rate.

CIBC is the result of Canada’s largest bank merger in history. It consisted of the Canadian Bank of Commerce, established in 1867, and the Imperial Bank of Canada, established in 1875. The merger took place on June 1, 1961. Later, CIBC entered into asset management with a stake in TAL Investment Counsel. However, the Canadian government blocked their plans to merge with TD bank in 1998.

This was followed by another failure when they attempted to merge with Manulife Financial in 2002. Talks fell apart when both parties realized they would not likely get approval from the government. Despite these mergers falling through, they did expand with the acquisition of Wood Gundy and Merrill Lynch Canada. Since 2010 CIBC has continued to expand with the acquisitions of multiple wealth management firms and has its sights set on expansion in the U.S.

No, CIBC tends to have much higher rates. For example, their five-year fixed rate was 6.49%, BMO was 5.09%, TD was 5.44%, and RBC was 5.69%.

You can apply online, via phone, or by appointment at your local branch or mobile bank advisor.

Considering CIBC is amongst the highest interest rates in Canada, it is worth trying to negotiate a better rate. You can reference similar mortgage products and features at other banks for leverage. Be sure to point out that they do not offer any break on payments.

Most mortgage-related questions are answered at their central number: 1-888-264-6843.

No, CIBC is the only big bank not offering a mortgage feature to pause your monthly mortgage payment. With its higher interest rates, it is not the best bank to consider, especially for first-time buyers.

In most cases, CIBC needs a credit score of at least 600 to qualify for a mortgage, but they often want your score to be even higher. This is particularly true if you are self-employed or have non-traditional sources of income such as commission, freelance work or owning your own business.

Yes, CIBC offers mortgage transfer options with potential cashback incentives for eligible borrowers.

Yes, CIBC offers mortgage transfer options with potential cashback incentives for eligible borrowers.

You can lock in your rate for up to 120 days by getting pre-approved through CIBC or Citadel Mortgages.

While 33% of non-homeowners believe they’ll never own*, our Citadel mortgage brokers are 100% confident they can make it happen. How? With our expert advice and guidance.

(5-years interest savings with Citadel Mortgages)**

(Interest savings with Citadel Mortgages)

(5-years interest savings with Citadel Mortgages)**

(Interest savings with Citadel Mortgages)

Choosing the right mortgage rate can significantly impact your financial future. At Citadel Mortgages, we help you compare CIBC mortgage rates with other top lenders to ensure you make the best decision. Contact us today to start saving and achieving your homeownership goals.

At Citadel Mortgages, we specialize in helping Canadians navigate the complexities of mortgage rates and terms. Whether you’re looking for a 6-month fixed rate, a 5-year variable, or something in between, our team is here to provide personalized guidance and access to the best rates in Canada.

See how you can save and become mortgage-free sooner

Calculate how much you’d spend each month to buy a home or renew or refinance your mortgage.

Discover how much cash back you could receive with our Cash Back Mortgage Calculator.